China’s credit rating was recently downgraded by Standard & Poor’s (SP Global) from AA- to A+ because of worries over the rapid growth of the country’s debt. Not surprisingly, China refuted concerns, with the China Ministry of Finance (MOF) saying that “the downgrade is a result of [SP Global’s] long-standing mode of thinking and misreading of the Chinese economy based on developed countries’ experience.”

What SP Global ignored, MOF says, is the country’s distinctive financing structure, the wealth-creating effect of government spending and its support for growth, as well as sound development fundamentals and growth potential.

Let’s assess the 2 key components of credit analysis: the willingness and ability to pay off debt, which are the focus on the sovereign default risk when the problem is corporate debt, and the fact that more than 90% of China’s debt is domestically funded meaning no foreign capital flight to precipitate a crisis and no impact on China’s future funding costs.

“China’s total debt to GDP at the end of 2016 stood at 257% of GDP. government debt was 46%, household was 44% and non-financial corporate debt stood at 166%”.–Edmund Harriss

SP Global’s downgrade specifically deals with the creditworthiness of Chinese Government Bonds which, at 46% of GDP equates to approximately $5.25 trillion of debt. The average yield on these bonds is 3.5% meaning an annual interest rate payment of ~$184 billion. Total fiscal revenue amounted to $3.2 trillion (28% of 2016 GDP). The government can easily service its debt so that’s not the problem.

However, corporate debt has grown rapidly in recent years and concerns are justified. There have been two drivers of this growth. The first was government efforts to boost GDP growth between 2008 and 2011; the second was the subsequent rise in lending by the banking sector, with excessive risk appetite underpinned by expectations of implicit guarantees which encouraged excessive borrowing.

The assumption that the government is on the hook for every dollar of corporate debt (which will continue to grow) and that China’s ability to repay it now comes into question. The counter-arguments are as follows: The government has already identified debts linked to government policy and is swapping those into municipal bonds – for example taking sovereign responsibility. Secondly, debt run up on private projects by both corporates and local governments are not their responsibility.

Consequently, we are now seeing more bond defaults. Banks are under intense regulatory pressure to shrink balance sheets and curb risk appetite and excess capacity industries (steel, cement, and real estate) all have limited access to capital as bank lending to these sectors is restricted by the central bank.

China Is Willing And Able

China is a country with a plan. Since the 1980s China has been on a course to maximize its resources to become an economic and geopolitical power house. China’s communists are not interested in the furtherance of Marxism but in the re-establishment of China’s wealth and power. They have embarked on a long program of industrialization, export manufacturing and now private consumption.

Having started out as a manufacturer of cheap clothing and toys, China is now the largest manufacturer of computers, smartphones and engineered goods; they have the world’s largest car market and plan to be the leader in new industries such as renewable energy and electric vehicle sectors.

“China has already demonstrated its commitment to change.”

In 1994 China nearly did go bust. Inflation hit 27%, fiscal revenue fell to 10% of GDP and the banking sector nearly collapsed. China began to dispense with the State-Owned enterprise model with cradle-to-grave benefits: 150,000 enterprises were closed; 25-30 million people were put out of work and the banking system was recapitalized to the tune of 20% of GDP.

Today, we believe that China is willing to stand by its obligations because there is a greater goal. We believe that China is NOT willing to bail out the banking sector yet again, without a change in banks’ behavior. This lies at the heart of China’s efforts to reduce leverage.

When it comes to ability, underlying China’s debt story is an economic transformation from low- to higher-end manufacturing accompanied by higher wages. An infrastructure investment program created the framework for China’s increasing productivity. Certainly, there has been waste as there are projects that will never pay for themselves. But at a macro-level China is becoming wealthier.

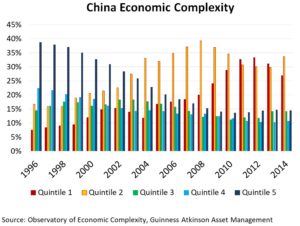

The path of economic transformation can be seen through a measure known as Economic Complexity. This combines the diversity of countries and the ubiquity of products to create measures of the relative complexity of a country’s exports.

Edmund Harriss is the investment director and a fund manager with Guinness Atkinson Asset Management. He is based in London.