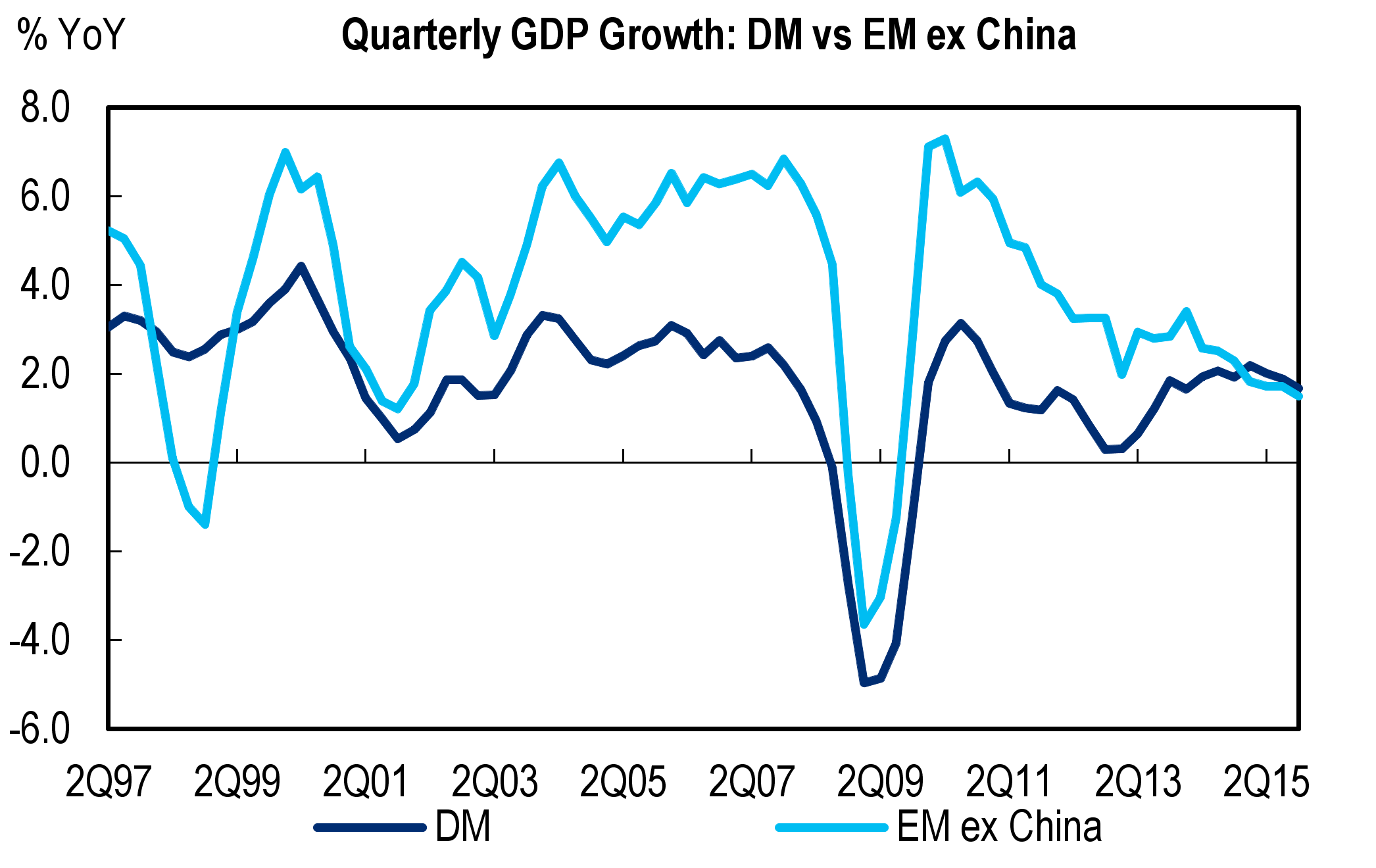

A period of exceptionally weak growth across emerging markets (EM) may be ending, but the current outlook is nothing to shout about. GDP growth in emerging markets (ex-China) fell below growth in developed markets late 2015, for the first time since 1998. This period of economic underperformance is now very likely to be coming to an end, largely due in part to the fact that growth in Russia and Brazil – whose deep recessions were at the root of EM’s weakness on average – probably have upside risks now, according to David Lubin, Citi’s London-based chief emerging markets economist.

Perhaps the most important piece of background for a more negative view about EM growth is the continuing recession in global trade. Global growth in regards to trade volumes was close to zero in early 2016, and it looks like EM exporters are underperforming their counterparts in developed markets (DM). The main problem lies in Asia, where export volume growth rate in the past six months has averaged -3%, Lubin wrote in a note to clients this month.

“One big underlying problem is that trade policy is moving in a worrying direction: the number of beggar-thy-neighbor measures implemented globally during the first four months of this year has exceeded anything we’ve seen in the equivalent period of recent years. Increasing localization requirements are playing an important role.”

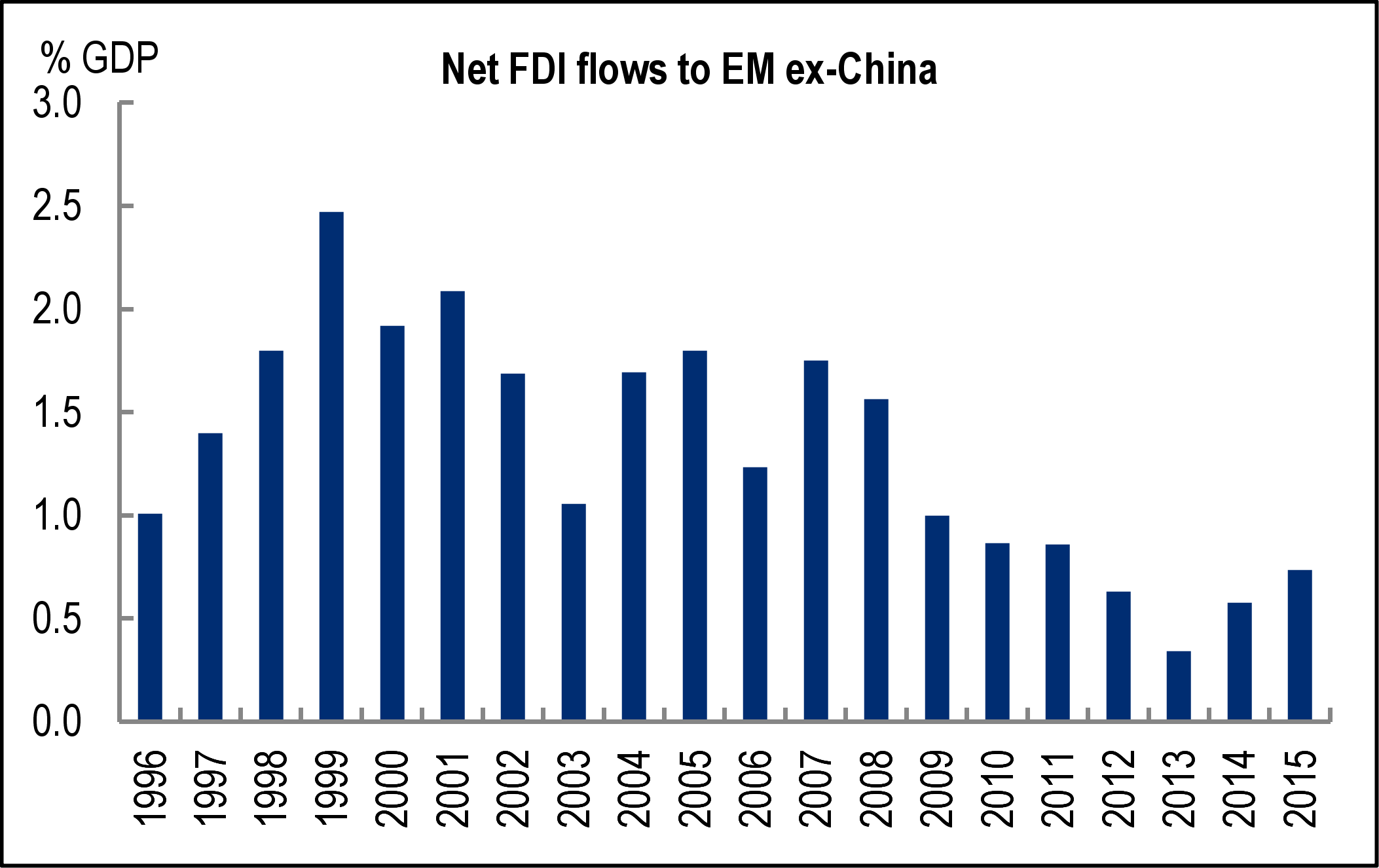

De-liberalizing trade policies may also have something to do with the ongoing weakness of foreign direct investment (FDI) flows to EM. In the four years since 2012, net FDI flows averaged just 0.6% GDP, down from 1.5% between 2002-2008. Weak trade growth and the decline in FDI flows to EM are related to each other in some kind of feedback loop and “both these phenomena should help ensure disappointing growth performance in EM,” Lubin said.

Meanwhile, investors are having to deal with what might be called the ‘oil price paradox’. One one hand, the stability of oil prices has helped to support risk appetite towards emerging markets. The credit space, for example, is now fully valued [in Citi’s view]. But on the other hand, the oil price is producing exactly the upside risks to inflation that might bring us closer to the biggest and most obvious threat to EM asset prices: US monetary tightening.

While a well-anticipated US hike will be less of a shock to EM than an unanticipated one, the weakness of EM growth probably increases EM’s sensitivity to the Fed.

Charts: Citi Research, IIF.