When India’s government suddenly withdrew the country’s two large currency denominations, the move was intended to combat black money, corruption and terrorism. But the results so far are chaos and uncertainty, as India’s small businesses and massive rural population struggle to adapt and questions remain about hidden “black money” untouched by the currency withdrawal.

Modi’s Surprise

In an unexpected move, the Indian government on November 8 the immediate withdrawal of the legal tender status of the country’s two largest currency denominations. Indian citizens have until the end of 2016 to trade their ₹500 and ₹1,000 rupee notes at banks and designated offices for a limited amount of cash in lower denominations (that limit was recently dropped from ₹4,500 per person to ₹ 2,000).

The remaining money will be credited to citizens’ bank accounts, provided they have valid proof of identity. The catch: While most Indians hold proof of identity after the introduction of the Aadhar card system in 2009, only about 15% use a bank account for transactions (Demirguc-Kunt et. al, 2015).

How big is the impact of this withdrawal? Chaos, confusion, long lines outside banks and even loss of life have resulted already. And the financial impact may grow.

At the time of the announcement, large denominations accounted for 87% of the ₹16,416 billion of currency circulating in the Indian economy. Some 39% of bills were ₹1000 and 48% were ₹500, according to Reserve Bank of India (RBI). Only around 15% was in smaller denominations.

Together, those ₹1,000 and ₹500 denominations amount to 10.4% of India’s GDP in 2015-2016, compared to just 3% in 2000-2001. This massive increase in the volume of large denominations, the government argues, reflects counterfeit currency and black money (untaxed money, which according to some estimates, constitutes 75% of India’s GDP) and money used to fund extremist and terrorist activities. The decision is aimed at stepping up the fight against these forces.

Thoughtful And Gradual Change Is Needed

A gradual and thoughtful initiation of this policy would have achieved this aim and brought other positive effects. A bank-centric payment system would help the government track money being exchanged, and thus better measure the economy—a major challenge in India, as in other developing countries.

A gradual change would also help improve the efficiency of the financial sector by reducing transaction costs and frictions. In India, corruption is rife in educational institutions and hospitals, including those in the private sector. A shift to formal transactions might help reduce the capitation fees charged for admissions and jobs in these institutions.

However, these benefits are unlikely to be achieved, even in the long run, thanks to the inadequate preparation for the currency withdrawal.

When the government withdrew 86% of liquidity from the economy overnight, it created chaos and the sense that this was an experiment with the life of the poor.

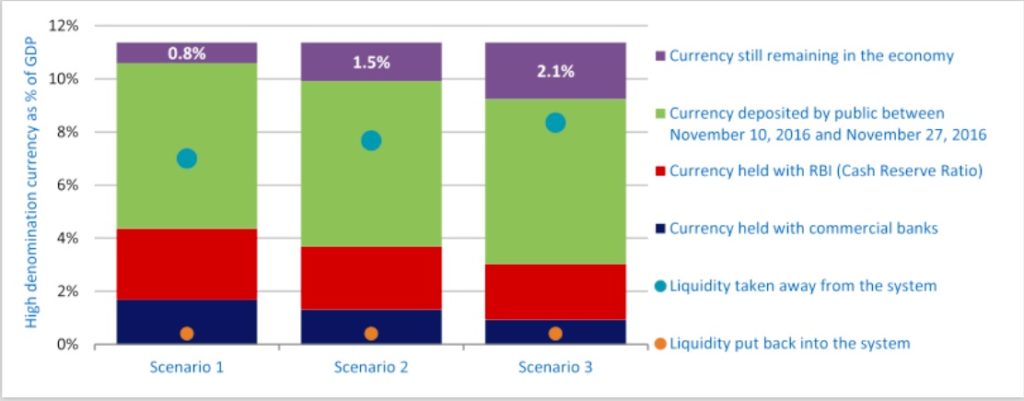

Early data on the cash exchanges allows for rough estimates of the magnitude of unaccounted cash stored in the high denominations. The total amount of high denomination currencies in circulation on November 8 was ₹15,441 billion, of which the amount deposited to banks between November 10-27 (including exchanges) was ₹8,449.82 billion. Note that the commercial banks in India require maintaining a portion of their deposit in cash – called the cash-deposit (CD) ratio – which was 6.53% in November. With a total deposit of ₹100,965 billion (as of Q2 2016-2017), the CD amounts to ₹6,593 billion.

Of this, banks must keep ₹4,039 billion (4% of their total deposit) as cash reserve (CR) with the Central Bank. The CR with the Central Bank is likely kept in high denomination, whereas the remaining ₹2,554 billion with commercial banks may include lower denominations.

Abdul A Erumban is based in Brussels, Belgium, as a senior economist with The Conference Board.

This is the second in our series of reporting on India’s demonetization.